Table of Contents

Quick Summary

- Pradhan Mantri Awas Yojana (PMAY) includes the Credit-Linked Subsidy Scheme (CLSS) for home loans.

- CLSS offers interest subsidy to Economically Weaker Section (EWS), Low Income Group (LIG), and Middle Income Group (MIG).

- Eligibility is based on total family income, not just the applicant’s earnings.

- The scheme supports home purchase, construction, extension, or conversion of kaccha houses into pucca homes.

- Eligible beneficiaries can avail up to 6.5% interest subsidy on home loans for a tenure of up to 20 years.

- Subsidy reduces the overall loan burden and monthly EMIs.

- PMAY aims to provide affordable housing for all eligible citizens.

- Subsidy approval and disbursal usually take around 3–4 months after verification.

Under the Pradhan Mantri Awas Yojana, there is a Credit Linked Subsidy Scheme, which is a component designed to offer an interest subsidy on home loans for eligible applicants. With the CLSS subsidy, a home buyer can take care of purchasing, construction and home improvement needs.

Key Highlights of the PMAY CLSS Subsidy include:

- The PMAY subsidy scheme is extended for the economically weaker, lower- and middle-income groups of the society. To be eligible for this subsidy, the government considers a family’s overall income and not just the applicant’s income.

- The primary goal of PMAY is to provide permanent housing for all eligible applicants by 2022.

- Applicants can avail an interest subsidy of 6.5% for up to 20 years, and the loan amount is based on the income group classification.

- Eligible applicants of this subsidy can use this benefit to either purchase a new home from a builder, construct one or upgrade to a pucca house if they are currently living in a kaccha house.

The PMAY CLSS subsidy makes the home loan process less expensive and taxing on the eligible applicants with its affordable housing facility.

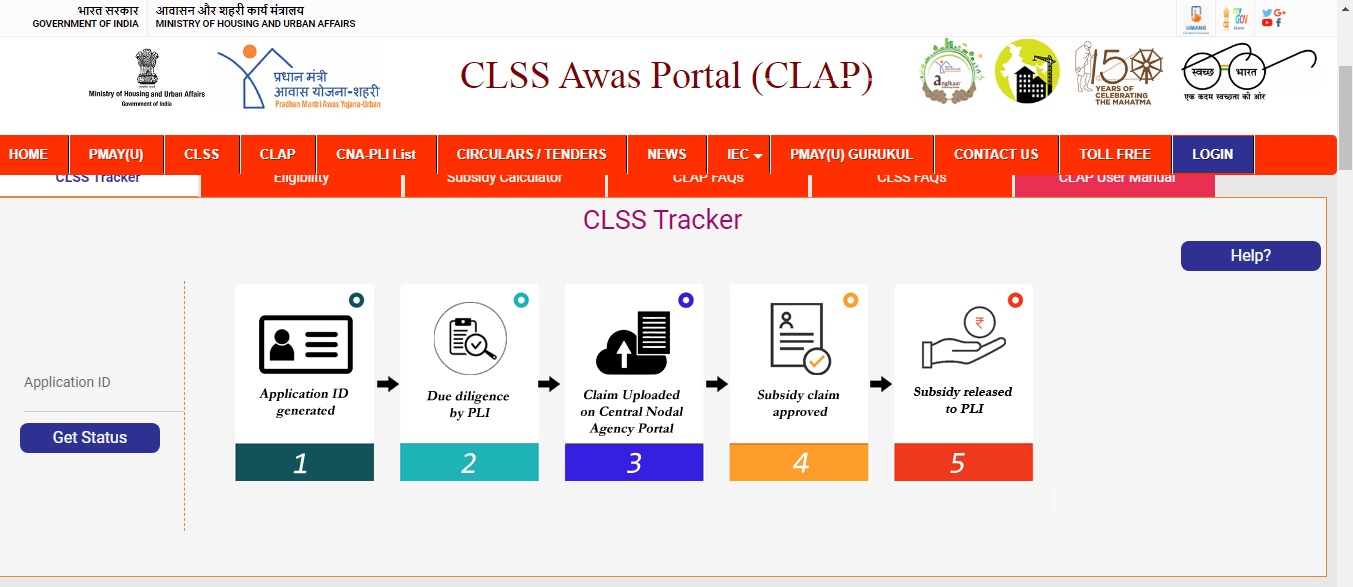

How to Track the PMAY Status for Assessment?

Courtesy - assets-news.housing.com

Applicants can easily track their PMAY application status online through the official government portal. To track the PMAY status:

1. Visit the official PMAY website

2. Click on the “Track Assessment Status” option

3. Choose one of the following methods: Track using Name, Father’s Name and Mobile Number or,

Enter the Assessment ID received during application.

This facility helps applicants monitor or track their application progress and stay updated on the subsidy approval process.

Income Categories & Required Documents for PMAY CLSS Subsidy

| Income Categories |

| EWS: Annual household income up to Rs 3 lakhs |

| LIG: Rs 3 lakhs to Rs 6 lakhs |

| MIG: Rs 6 lakhs to Rs 12 lakhs |

| MIG II: Rs 12 lakhs to Rs 18 lakhs |

| Documents Required |

| Aadhaar Card |

| PAN Card |

| Income proof |

| Property documents |

| Loan sanction letter |

| Bank statements |

How Long does it take to get a PMAY CLSS Subsidy?

Once you have shared all your details with the government, you need to wait until they are verified. Typically, the PMAY CLSS subsidy process takes around 3-4 months after successful verification. Only then will your Pradhan Mantri Awas Yojana process begin.

Here is how it works:

- Two central nodal agencies, namely the Housing & Urban Development Corporation (HUDCO) and National Housing Bank (NHB), are in charge of releasing the interest subsidy under PMAY.

- The NHB reviews applications and conducts due diligence and data validation before approving subsidy payments for eligible borrowers.

- After applying for the PMAY Credit-Linked Subsidy Scheme, the borrower will receive an application ID, which helps track the PMAY application status. From submitting the PMAY home loan application to the bank or a lending institution to getting the subsidy release, the application ID is essential at almost every stage.

- After the subsidy is released, it is credited directly to the home loan account of the beneficiary. Applicants should verify the credit in their loan account statement.

- Once the PMAY CLSS subsidy amount is credited, the outstanding principal of the home loan reduces, which results in lower EMI.

Conclusion

The PMAY CLSS subsidy schemes play an important role in improving access to affordable housing in India and also institutional credit flow by intervening on the demand side to help the lower- and middle-income groups buy a home. With the introduction of this subsidy, more and more people have been able to realise their dream and avail affordable housing in India.

FAQs on How Much Time It Takes to Get a PMAY CLSS Subsidy

01. What is the PMAY Credit-Linked Subsidy Scheme (CLSS)?

CLSS is a PMAY component that provides interest subsidy on home loans to eligible income groups.

02. Who is eligible for the PMAY CLSS subsidy?

EWS, LIG, and MIG families meeting income and housing eligibility criteria can apply.

03. How much subsidy is available under PMAY CLSS?

Beneficiaries can get up to 6.5% interest subsidy depending on their income category.

04. How long does PMAY subsidy approval take?

The subsidy is usually credited within 3–4 months after document verification.

05. How can I track my PMAY subsidy status?

You can track it online using your assessment ID or personal details on the PMAY portal.

Author – Expert Review

Shekhar J. Parikh – Co Founder – Gharpedia | Director – SDCPL

Shekhar J. Parikh – Co Founder – Gharpedia | Director – SDCPL

This article has been reviewed for technical and execution accuracy by Shekhar J. Parikh, Director and Consulting Engineer at Sthapati Designers & Consultants Pvt. Ltd. With over 40 years of experience in civil engineering, project execution, and construction management across Gujarat and Maharashtra, he ensures the content reflects practical site knowledge, quality control standards, and industry best practices, while also supporting informed decision-making for property buy, sell, and rent considerations.

Find him on: LinkedIn